THE PROBLEM OF THE RUPEE:

ITS

ORIGIN AND ITS SOLUTION

(HISTORY OF INDIAN CURRENCY & BANKING)

_________________________________________________________________________________________________

CHAPTER VIl

A

RETURN TO THE GOLD STANDARD

We have examined the exchange standard in the light of the claim made on behalf of it, that it is capable of maintaining the gold parity of the rupee. This was the criterion laid down by the Chamberlain Commission as a fitting one by which to judge the merits or demerits of that standard. But is the adequacy of that criterion beyond dispute ? In other words, supposing the rupee has maintained its gold parity, which it has only as often as not, does it follow that all the purposes of a good monetary system are therefore subserved ?

In the exchange standard, " as the system is now operated, the coinage is manipulated to keep it at par with gold "[f1] as though money is only important for the amount of gold it will procure. But what really concerns those who use money is not how much gold that money is worth, but how much of things in general (of which gold is an infinitesimal part) that money is worth. Everywhere, therefore, the attempt is to keep money stable in terms of commodities in general, and that is but proper, for what ministers to the welfare of people is not so much the precious metals as commodities and services of more direct utility. Stability of a currency in terms of gold is of importance only to the dealers in gold, but its stability in terms of commodities in general affects all, including the bullion-dealers. Even Prof. Keynes, in his testimony before the Indian Currency Committee of 1919, observed[f2]—

"I should aim always... at keeping Indian prices stable in relation to commodities rather than in relation to any particular metallic or particular foreign currency. That seems to me of far greater importance to India." It is, of course, a little difficult to understand how the remedy of high exchange which he supported was calculated to achieve that object. Raising the exchange was a futile project, in so far as it was not in keeping with the purchasing power of the rupee. As an influence governing prices it could hardly be said to possess the virtue he attributed to it. The existing price-level it could affect in no way; nor could a high exchange prevent a future rise of prices. It could only change the base from which to measure prices. Future prices could vary as easily from the new high base-line as prices did in the past from the old baseline. In other words, Mr. Keynes seems to have overlooked the fact that exchange was only an index of the price-level, and to control it, it was necessary to control the price-level and not merely give it another name which it cannot bear and will not endure, as was proved in 1920 when the rupee was given in law the value of 2s. (gold) when in practice it could not fetch even 1s. 4d. sterling, with the result that the rupee exchange sank to the level determined by its purchasing power. But, apart from this question, we have the admission of the ablest supporter of the exchange standard that the real merit of a currency system lies in maintaining the standard of value stable in terms of commodities in general.

Given that this is the proper criterion by which to judge a currency system, we must ask what has been the course of prices in India since the Mint closure in 1893? This is a fundamental question, and yet not one among the many who have praised the virtues of the exchange standard has paid any attention to it. In vain may one search the pages of Prof. Keynes, Prof. Kemmerer, or Mr. Shirras for what they have to say of the exchange standard from this point of view. The Chamberlain Commission or the Smith Committee on Indian currency never troubled about the problem of prices in India, [f3]and yet without being satisfied on that score it is really difficult to understand how anyone can give an opinion of any value as to the soundness or otherwise of that standard.

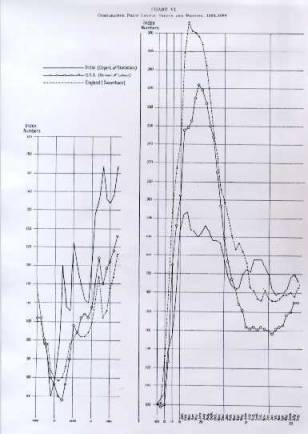

In proceeding to consider the exchange standard from the standpoint of prices, it is as well to premise that one of the important reasons why the Indian Mints were closed to the free coinage of silver was that the rupee was a depreciating currency resulting in high prices.[f4] The closing of the Mints, therefore, should have been followed by a fall of prices in India; for, to adopt the phraseology of Prof. Fisher,[f5] the pipe-connection between the money reservoir and the silver-bullion reservoir was owing to the Mint closure cut off or stopped, thereby preventing the passage of silver from the bullion reservoir to the money reservoir. In other words, the newly mined silver could not become money after the Mint closure and lower the purchasing power of the rupees in circulation. If this is so, then how very disappointing has been the effect of the Mint closure ! From the standpoint of prices the rupee has become a problem as it had never been before. The rise of prices in India since the Mint closure (See Chart VI) has been quite unprecedented in the history of the country.

Indeed, the rise of prices in India before the Mint closure, when the pipe-connection between the silver-bullion reservoir and the rupee-currency reservoir was intact, must be regarded as very trifling compared with the rise of prices after the Mint closure when the pipe-connection was cut off. From the standpoint of prices the Mint closure has therefore turned out to be a curse rather than a blessing, and literally so, for, under an ever-rising price-level, life in India is rendered quite unbearable. No people have undergone so much misery owing to high prices as the Indian people have done. During the war period the price-level reached such a giddy height that the reports of suicide by men and women who were unable to buy food and clothing were in no way few and far between. It may, however, be argued that the rise of prices in India would have been greater if the Mints had not been closed and India had remained a purely silver-standard country. A good deal, no doubt, can be said in favour of this view. It is absolutely true that silver, being universally discarded, has become unfit for functioning as a standard of value. To that extent an exchange standard is better than a pure-silver standard. But is it as good as a gold standard ?

On the basis of the doctrine of purchasing power parities as an explanation of actual exchange rates, one may be led to answer the question in the affirmative. For it may be argued that if the gold value of the rupee was maintained it is because gold prices and rupee prices were equal.[f6] This, it may be said, is all that the exchange standard aims at doing and can be claimed to have done, for the fact that the gold-standard reserve was seldom depleted is a proof that the general prices inside India were on the same level as those ruling outside India. On a priori considerations such as these, the exchange standard may be deemed to be as good as a gold standard.

One may ask as to why Indian prices should have been kept as high, if they were no higher than gold prices, and whether it would not have been better to have kept Indian prices on a lower level. But we shall not raise that question. We shall be satisfied if Indian prices were only as high as gold prices. Now did Indian prices rise only as much as gold prices ? A glance at the chart reveals the surprising phenomenon that prices in India not only rose as much as gold prices, but rose more than gold prices. Of course in comparing Indian prices with gold prices to test the efficacy of the exchange standard we must necessarily eliminate the war period, for the reason that gold had been abandoned as a standard of value by most of the countries. And, even if we do take that period into account, it does not materially affect the conclusion, for although India was not a belligerent country, yet prices in India were not very much lower than prices in countries with most inflated currencies during the war, and barring a short period were certainly higher than gold prices in U.S.A.

It is obvious that the facts do not agree with the a priori assumption made in favour of the exchange standard. So noticeable must be said to be the local rise in Indian prices above the general price level in England that even Prof. Keynes, not given to exaggerate the faults of the exchange standard, was, as a result of his own independent investigation, convinced that[f7]

"a comparison with Sauerbeck's index number for the United Kingdom shows that the change in India is much greater than can be accounted for by changes occurring elsewhere."

What is then the explanation of this discrepancy between the a priori assumption and the facts of the case. The explanation is that the actual exchange rates correspond to the purchasing power parities of two currencies not with regard to all commodities but with regard to some only. In this connection it is better to re-state the doctrine of the relation of the purchasing power parities to exchange rates with the necessary qualification. A rigorously strict formulation of the doctrine should require us to state that Englishmen and others value Indian rupees inasmuch as and in so far as those rupees will buy such Indian goods as Englishmen want; while Indians value English pounds inasmuch as and in so far as those pounds will buy such English goods as the Indians want. So stated it follows that the actual exchange rates are related to purchasing power parities of the two currencies with regard to such commodities only as are internationally traded. To assume that the actual exchange rate is an exact index of the purchasing power parity of the two currencies with regard to all the commodities is to suppose that the variations in the purchasing power of a currency over commodities which are traded and which are not traded are the same. [f8]There is certainly a tendency for movements in the prices of these two classes of goods to influence one another in the long run; so that it becomes possible to say that the exchange value of a currency will be determined by its internal purchasing power. The doctrine of purchasing power parity as an explanation of exchange rates is valuable as an instrument of practical utility for controlling the foreign exchanges and it is as such that the doctrine was employed in an earlier portion of this study to account for the fall in the gold value of the rupee. But to proceed, on the basis of this relationship between the purchasing power of a currency and its exchange value, to argue that at any given time the exchange is more or less an exact measure of general purchasing power of the two currencies, is to assume what cannot always be true, namely, that the prices of traded and non-traded goods move in sympathy. This assumption is too large and can only be said to be more or less true according to circumstances. Now as Prof. Kemmerer[f9] points out :—

"While India's exports and imports in the absolute are large, still, in the main, the people of India live on their own products, and a large part of those products run their life history from production to consumption in a very small territory. They have only the remotest connection with foreign trade, gold, and the gold exchanges. In time, of course, any substantial disturbance in the equilibrium of values in the country's import and export trade will make itself felt in these local prices, but allowing for exceptions, it may be said that in a country like India the influences of such disturbances travel very slowly and lose much of their momentum in travelling."

In consequence of the thinness of connection between the two it is obvious that the prices of such Indian goods as do enter into international trade cannot always be said to move in more or less the same proportion as those which do not. Besides this thinness of connection which permits of deviations of the general purchasing power of a currency from the level indicated by the actual exchange rate, it is to be noted that the prices of Indian commodities which largely enter into international trade are not governed by local influences. Such exports of India as wheat, hides, rice and oil seeds are international commodities, not solely amenable to influences originating from changes that may be taking place in the prices of home commodities and services. The combined effect of these two circumstances, except in abnormal events such as the war, is to militate against the prices of traded and non-traded goods moving in quick sympathy[f10]

If this is true, then, although the maintenance of the exchange standard does imply a purchasing power parity of the rupee with gold, it is not a purchasing power parity of the two currencies with respect to all the commodities. All that it implies is that the purchasing power of the rupee over such commodities as entered into international trade was on a par with gold, so that there did not often arise the necessity of exhausting the gold reserve. The preservation of the gold reserve only meant that there was equality of prices so far as internationally traded goods were concerned. Thus interpreted, the fact that the rupee maintained its gold value does not preclude the possibility of Indian prices being, on the whole, higher than gold prices, thereby vitiating the a priori view that the exchange standard is as good as the gold standard.

It should be pointed out[f11] that all changes of prices affect more or less the welfare of the individual. However, the general flexibility of the modern economic organisation, with its mobility of capital and labour, free competition, power of choice, inventive genius and intellectual resources of enterpreneurs and merchants, takes care of the normal and temporary fluctuations of prices. But when a change in the price-level is general and persistent in one direction the case is otherwise. Arrangements based on the expectation that the price movement is only temporary, and that there will be a return to the former normal position, constantly come to naught. Suffering endured in holding on for the turn in the movement cannot be offset by gains in another. In short, such a persistent price movement in one direction is bound to confound ordinary business sagacity and so vitiate all calculations for the future as to result in unlimited dislocation or loss and subject the individual to such powerful and at the same time incalculable influences that his economic welfare cannot but escape entirely from his control, and prudence, forethought, and energy become of no avail in the struggle for existence. Perfect stability of value in a monetary standard is as yet only an ideal. 'But the evil consequences of instability are so great that Prof. Marshall, believing as he did that the general prejudice against tampering with the monetary foundations of economic life was a healthy prejudice, yet observed that much may be done towards safeguarding the economic welfare of communities by lessening its variability.[f12] A depreciating standard of value, as gold has been since 1896, is an evil. But can a standard of value, undergoing a continuous depreciation as has been the case with the exchange standard, and that too of a greater depth than the gold standard—in other words, causing a greater rise of prices—be regraded as a good standard of value ?

In the light of this it is strange that Prof. Keynes, in his treatise on Indian Currency and Finance, should have maintained that the exchange standard contained an essential element in the ideal standard of the future[f13]—a view subsequently endorsed by the Chamberlain Commission. If stability of purchasing power in terms of commodities in general is the criterion for judging a system of currency, then few students of economics will be found to agree with Prof. Keynes. Perhaps it is not too sanguine to say that even the Prof. Keynes of 1920 will prefer a gold standard to a gold-exchange standard, for under the former prices have varied much less than has been the case under the latter.

In this connection attention may be drawn to the prevalent misconception that India is a gold-standard country. It will be admitted that the best practical test whether any two countries have the same standard of value is to be found in the character of the movements in their price-levels. So sure is the test that Prof. Mitchell, after a very careful and wise survey of the price-level of different countries and the American price-level during the greenback period, was led to observe[f14] that

"when two countries have a similar monetary system and important business relations with each other, the movements of their price-levels as represented by index-numbers are found to agree rather closely. This agreement is so strong that similarity of movement is usually found even when comparisons are made with material so crude as index-numbers compiled from unlike lists of commodities and computed on the basis of actual prices in different years."

Now, we know that before the war England was a gold-standard country, and we also know that there was no close correspondence between the contemporary movements of the price-levels of India and England. In view of this, it is only a delusion to maintain that India has been a gold-standard country. On the other hand, it is better to recognise that India has yet to become a gold-standard country unless we are to fall into the same error that Prof. Fisher*[f15] must be said to have committed in attributing the extraordinary rise of prices in India to the existence of a gold standard, when, as a matter of fact, it should have been attributed to the want of a gold standard.

How can she become a gold-standard country ? The obvious answer is, by introducing a gold currency. Prof. Kenyes scoffs at the view that there cannot be a gold standard without a gold currency as pure nonsense[f16] He seems to hold that a currency and a standard of value are two different things. Surely there he is wrong. Because a society needs a medium of exchange, a standard of value, and a store of value to sustain its economic life, it is positively erroneous to argue that these three functions can be performed by different instrumentalities. On the other hand, as Professor Davenport insists[f17]

" all the different uses of money are merely different aspects or emphasis of the intermediate function. Deferred payments...... are merely deferred payments of the intermediate. So again of the standard aspect; whatever is the general intermediate is by that fact the standard. The functions are not two, but one...... Clearly, also, the intermediate may be a storehouse of purchasing power. The second half of the barter may be deferred. The intermediate is generalised purchasing power. Delay is one of the privileges which especially the intermediate function carries with it."

Thus the rupee by reason of being the currency is also the standard of value. If we wish to make gold the standard of value in India we must introduce it into the currency of India. But it may be asked what difference could it make to the price level in India if gold were made a part of the Indian currency ? To answer this question it is necessary to lay bare the nature of the rupee currency. Now it will be granted that a standard of value which is capable of expansion as well as contraction is likely to be more stable than one which is incapable of (such a manipulation. The rupee currency is capable of)[f18] easy expansion, but is not capable of easy contraction by reason of the fact that it is neither exportable nor meltable, nor is it convertible at will. The effects, of such a currency as compared with those of an exportable currency were well brought out by the late Hon. Mr. Gokhale in a speech in which he observed.[f19]

" Now, what is the difference if you have an automatic self-adjusting currency, such as we may have with gold or we had with silver before the year 1893, and the kind of artificial currency that we have at present ? Situated as India is you will always require, to meet the demands of trade, the coinage of a certain number of gold or silver pieces, as the case may be, during the export season, that is for six months in the year. When the export season is brisk money has to be sent into the interior to purchase commodities. That is a factor common to both situations, whether you have an artificial currency, as now, or a silver currency, as before 1893. But the difference is this. During the remaining six months of the slack season there is undoubtedly experienced a redundancy of currency, and under a self-adjusting automatic system there are three outlets for this redundancy to work itself off. The coins that are superfluous may either come back to the banks and to the coffers of Government, or they may be exported, or they may be melted by people for purposes of consumption for other wants. But where you have no self-adjusting and automatic currency, where the coin is an artificial token currency, such as our rupee is at the present moment, two out of three of these outlets are stopped. You cannot export the rupee without heavy loss, you cannot melt the rupee without heavy loss, and consequently the extra coins must return to the banks and coffers of the government or they must be absorbed by the people. In the latter case the situation is like that of a soil which is water-logged, which has no efficient drainage, and the moisture from which cannot be removed. In this country the facilities for banking are very inadequate, and therefore our money does not swiftly return back to the banks or Government Treasuries. Consequently, the extra money that is sent into the interior often gathers here and there like pools of water turning the whole soil into a marsh. I believe the fact cannot be gainsaid that the stopping of two outlets out of the three tends to raise prices by making the volume of currency redundant."

Had gold formed a part of the Indian currency it would have not only met the needs for expansion but would have permitted contraction of currency in a degree unknown to the rupee. Gold would be superior to the rupee as a standard of value for the reason that the former is expansible as well as contractible, while the latter is only expansible but not contractible. This is merely to state in different language what has already been said previously, that the Indian monetary standard, instead of being a gold or a gold-exchange standard, is in all essentials an inconvertible rupee standard like the paper pound of the Bank Suspension period, and the extra local rise of prices which in itself an inconvertible proof of the identity of the two systems, is characteristic of both, is, to use the language of the Bullion Report[f20]

" the effect of an excessive quantity of a circulating medium in a country which has adopted a currency not exportable to other countries, or not convertible at will into a coin which is exportable."

Therefore, if some mitigation of the rise in the Indian price-level is desirable, then the most essential thing to do is to permit some form of "exportable" currency such as gold to be a counterpart of the Indian monetary system.

The Chamberlain Commission expended much ingenuity in making out a case against a gold currency in India.[f21] The arguments it urged were : (1) Indian people will hoard gold and will not make it available in a crisis: (2) that India is too poor a country to maintain such an expensive money material as gold ; (3) that the transactions of the Indian people are too small to permit of a gold circulation; and (4) paper convertible into rupees is the best form of currency for the people of India as being the most economical, and that the introduction of a gold currency will militate against the popularity of notes as well as of rupees. The bogy of hoarding is an old one, and would really be an argument of some force if hoarding was something which knew no law. But the case is quite otherwise. Money, being the most saleable commodity and the least likely, in a well-ordered monetary system, to deteriorate in value during short periods, is hoarded continually by all people, i,e, treated as a store of value. But in treating it as a store of value the possessor of money is comparing the utilities he can get for the money, by disposing of it now, with those he believes he can get for it in the future, and if the highest present utility is not so great as the highest future utility, discounted for risk and time, he will hoard the money. On the other hand, he will not hoard the money if the present use was greater than the future use. That being so, it is difficult to understand why hoarding should be an objection to a gold currency for the Indian people. If they hoard gold that means they do not care to spend it on current purchases or that they have another form of currency which is inferior to gold and which they naturally like to part with first. On the other hand, if they do wish to make current purchases and have no other form of currency they cannot hoard gold. There are instances when precious metals have been exported from India, when occasion had called for it,[f22] showing that the hoarding habit of the Indian peoples is not such an unknown quantity as is often supposed, and if on some occasions[f23] they hoarded an exportable currency when they should have released it, it is not the fault of the people but of the currency system in which the component parts of the total stock of money are not equally good as a store of value. The argument from hoarding, if it is an argument, can be used against any people, and not particularly against the Indian people.

The second argument against a gold currency in India has no greater force than the first. If gold were to disappear from circulation then the cause can be nothing else but the over-issue of another kind of money. In the nineties, when the question of establishing a gold standard in India was being considered, some people used to point to the vain efforts made by Italy and the Austrian Empire to promote the circulation of gold. That their gold used to disappear is a fact, but it was not due to their poverty. It was due to their paper issues. Any country can maintain a gold currency provided it does not issue a cheaper substitute.

Again, if gold will not circulate because transactions are too small the proper conclusion is not that there should be no gold circulation but that the unit of currency should be small enough to meet the situation. The difficulties of circulation raises a problem of coinage. But the considerations in respect of coinage cannot be allowed to rule the question as to what should be the standard of value. If the sovereign does not circulate it cannot follow that India should not have a gold currency. It merely means that the sovereign is too large for circulation. The case, if at all there is one, is against the sovereign as a unit and not against the principle of a gold currency. If the sovereign is not small enough the conclusion is we must find some other coin to make the circulation of gold effective.

The fourth argument against a gold currency is one of fact, and can be neither proved nor disproved except by an appeal to evidence whether or not gold currency has the tendency ascribed to it. But we may ask, is there no danger in a system of currency composed of paper convertible into rupees ? Will the paper have no effect on the value of the rupee ? The Commission, if it at all considered that question, which is very doubtful, was perhaps persuaded by the view commonly held, that as the paper currency was convertible it could not affect the value or the purchasing power of the rupee. In holding this view it was wrong ; for, the convertibility of paper currency to the extent it is uncovered does not prevent it from lowering the value of the unit of account into which it is convertible, because by competition it reduces the demand for the unit of account and thus brings about a fall in its value. Thus the paper, although economical as a currency, is a danger to the value of the rupee. This danger would have been of a limited character if the rupee had been freely convertible into gold. But the danger of a convertible paper currency to the value of a unit of account becomes as great as that of an inconvertible paper currency if that unit is not protected against being driven below the metal of ultimate redemption by free convertibility into that metal.[f24] The rupee is not protected by such convertibility, and as the Commission did not want that it should be so protected it should have realised that it was as seriously jeopardizing the prospects of the rupee being maintained at par with commodities in general, and therefore with gold, by urging the extension of a paper currency, be it ever so perfectly convertible, as it could have done by making the paper altogether inconvertible. But so observed was the Commission with considerations of economy and so reckless was it with considerations of stability of value, that it actually proposed a change in the basis of the Indian paper currency from a fixed issue system to that of a fixed proportion system.[f25] That, at the dictates of considerations of economy, the Commission should have neglected to take account of this aspect of the question, is only one more evidence of the very perfunctory manner in which it has treated the whole question of stability of purchasing power so far as the Indian currency was concerned.

If there is any force in what has been urged above, then surely a gold currency is not a mere matter of "sentiment" and a " costly luxury," but a necessity dictated by the supreme interest of steadying the Indian standard of value, and thereby to some extent, however slight, safeguarding the welfare of the Indian people from the untoward consequences of a rising price-level.

We now see how very wrong the Chamberlain Commission was from every point of view in upholding the departure from the plan originally outlined by the Government of India and sanctioned by the Fowler Committee. But that raises the question : How did that ideal come to be so ruthlessly defeated ? If the Fowler Committee had proposed that gold should be the currency of India, how is it that gold ceased to be the currency ? It cannot be said that the door is closed against the entry of gold, for it has been declared legal tender. Speaking in the language of Prof. Fisher, the movement of gold in the money reservoir of India is allowed a much greater freedom so far as law is concerned than can be said of silver. Silver, in the form of rupees, is admitted by a very narrow valve which gives it an inlet into that reservoir, but there is no outlet provided for it. On the other hand, gold is admitted into the same reservoir by a pipe-connection which gives it an inlet as well as an outlet. Why, then, does not gold flow into the currency reservoir of India ? A proper understanding on this question is the first step towards a return to the sound system proposed in 1898.

On an examination of the literature which attempts to deal with this aspect of the question, it will be found that two explanations are usually advanced to account for the non-entry of gold into the currency system of India. One of them is the sale of council bills by the Secretary of State. The effect of the sale of council bills, it is said, is to prevent gold from going to India. Mr. Subhedar, said to be an authority on Indian currency, in his evidence before the Smith Committee (Q.3,502), observed:—

"Since 1905 it has been the deliberate attempt of those who control our currency policy to prevent gold going to India and into circulation."

The council bill has a history which goes back to the days of the East India Company. [f26]The peculiar position of the Government of India, arising from the fact that it receives its revenues in India and is obliged to make payments in England, imposes upon it the necessity of making remittances from India to England. Ever since the days of the East India Company the policy has been to arrange for the remittance in such a way as to avoid the transmission of bullion. Three modes of making the remittance were open to the Directors of the East India Company: (1) sending bullion from India to England; (2) receiving money in England in return for bills on the Government of India; and (3) making advances to merchants in India for the purchase of goods consigned to the United Kingdom and repayable in England to the Court of Directors of the Company to whom the goods were hypothecated. Out of these it was on the last two that greater reliance was placed by them. In time the mode of remittance through hypothecation of goods was dropped " as introducing a vicious system of credit, and interfering with the ordinary course of trade." The selling of bills on India survived as the fittest of all the three alternatives,[f27] and was continued by the Secretary of State in Council—hence the name, council bill—when the Government of India was taken over by the Crown from the Company. In the hands of the Secretary of State the council bill has undergone some modifications. The sales as now effected are weekly sales,[f28] and are managed through the Bank of England, which issues an advertisement on every Wednesday on behalf of the Secretary of State for India, inviting tenders to be submitted on the following Wednesday for bills payable on demand by the Government of India either at Bombay, Madras, or Calcutta. The minimum fraction of a penny in the price at which tenders of bills are received has now[f29] been fixed at 1/32nd of a penny. The council bill is no longer of one species as it used to be. On the other hand there are four classes of bills: (1) ordinary bills of exchange, sold every Wednesday, known as " Councils " ', (2) telegraphic transfers, sold on Wednesdays, called shortly " Transfers "[f30] (3) ordinary bills of exchange, sold on any day in the week excepting Wednesday, called " Intermediates " ', and (4) telegraphic transfers, sold on any day excepting Wednesday, named " Specials." Now, in what way does the Secretary of State use his machinery of council bills to prevent gold from going to India ? It is said that the price and the magnitude of the sale are so arranged that gold does not go to India. Before we examine to what extent this has defeated the policy of the Fowler Committee, the following figures (Tables LI and LI I, pp. 579 and 582) are presented for purposes of elucidation.

From an examination of these tables two facts at once become clear. One is the enormous amount of council bills the Secretary of State sells. Before the closing of the Mints the sales of council bills moved closely with the magnitude of the home charges, and the actual drawings did not materially deviate from the amount estimated in the Budget. Since the closure of the Mints the drawings of the Secretary of State have not been governed purely by the needs of the Home Treasury. Since the closure, the Secretary of State has endeavoured[f31]—

"(1) To draw from the Treasuries of the Government of India during the financial year the amount that is laid down in the Budget as necessary to carry out the Ways and Means programme of the year.

TABLE LI

balance oF trade, coUNCIL drawings aND imports oF gold BEFORE 1893

Years. |

Balance of Trade (Mer. chandise: Private Account). |

Amount of Council

•Bills drawn. |

Excess ( +

) or Deficiency (—) of Bills drawn as compared with Budget Estimate. |

Home Charges. |

Cash Balances in the Home Treasury. |

Minimum Rate for

Council Bills. |

||

|

|

Gold. |

Silver. |

|

|

|

|

|

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

(7) |

(8) |

(9) |

|

£ |

£ 000,000 |

£ 000,000 |

£ |

£ |

£ |

£ |

|

1870-71 |

20,863,000 |

2.13 |

.9 |

— |

— |

10,031,261 |

3,305,972 |

1 l0 1/4 |

1871-72 |

31,094,000 |

3.43 |

6.3 |

— |

— |

9,703,235 |

2,821,091 |

l

10 3/8 |

1872-73 |

23,376,000 |

2.41 |

.7 |

13,939,095 |

+

939,095 |

10,248,605 |

2,998,444 |

1 10 3/8 |

1873-74 |

21,160,000 |

1.29 |

2.3 |

13,285,678 |

- 214,322 |

9,310,926 |

2,013,638 |

1 9 1/2 |

1874-75 |

20,137,000 |

1.73 |

4.3 |

10,841,615 |

+

841,615 |

9,490,391 |

2,796,370 |

1 9 3/4 |

1875-76 |

19,204,000 |

1.40 |

1.4 |

12,389,613 |

-1,910,387 |

9,155,050 |

919,899 |

1 9 |

1876-77 |

23,5.73,000 |

-18 |

6.1 |

12,695,800 |

- 964,200 |

13,851,296 |

2,713,967 |

1 6 1/2 |

1877-78 |

23,758,000 |

.41 |

12.7 |

10,134,455 |

-2,115,545 |

14,048,350 |

1,076,657 |

1 8 3/16 |

1878-79 |

23,167,000 |

.74 |

3.3 |

13,948,565 |

-3,051,435 |

13,851,296 |

1,117,925 |

1 6 5/8 |

1879-80 |

26,046,000 |

1.45 |

6.5 |

15,261,810 |

+

261,810 |

14,547,664 |

2,270,107 |

1 7 |

1880-81 |

21,464,000 |

3.03 |

3.2 |

15,239,677 |

-1,660,323 |

14,418,986 |

4,127,749 |

1 7 1/2 |

1881-82 |

32,855,000 |

4.02 |

4.5 |

18,412,429 |

+1,212,429 |

14,399,083 |

2,620,909 |

1 7 3/8 |

1882-83 |

31,389,000 |

4.01 |

6.1 |

15,120,521 |

- 221,479 |

14,101,262 |

3,429,874 |

1 7 |

1883-84 |

23,611,600 |

4.44 |

5.2 |

17,599,805 |

+1,299,805 |

15,030,195 |

4,113,221 |

1 7 1/4 |

1884-85 |

20,034,100 |

3.76 |

5.8 |

13,758,909 |

-2,741,091 |

14,100,982 |

2,249,378 |

1 6 3/4 |

1885-86 |

21,344,200 |

2.10 |

8.8 |

10,292,692 |

-3,481,008 |

14,014,733 |

4,726,585 |

1 5 7/8 |

1886-87 |

19,844,800 |

1.58 |

5.2 |

12,136,279 |

-1,195,121 |

14,409,949 |

5,280,829 |

1 4 1/8 |

1887-88 |

18,724,400 |

2.10 |

6.5 |

15,358,577 |

- 891,423 |

15,389,065 |

5,900,697 |

1 4 3/8 |

1888-89 |

20,271,900 |

1.92 |

6.3 |

14,262,859 |

+

262,859 |

14,983,221 |

3,259,933 |

1 4 |

1889-90 |

24,557,800 |

3.18 |

7.6 |

15,474,496 |

+

784,596 |

14,848,923 |

5,402,873 |

1 4 |

1890-91 |

20,733,800 |

4.25 |

10.7 |

15,969,034 |

+

980,034 |

15,568,875 |

3,885,050 |

1 4 15/16 |

1891-92 |

27,632,400 |

1.68 |

6.3 |

16,093,854 |

+

93,854 |

15,874,699 |

4,122,626 |

1 3 1/16 |

1892-93 |

29,287,300 |

1.75 |

8.0 |

16,532,215 |

- 467,785 |

16,334,541 |

12,268,388 |

1 2 5/8 |

" (2) To draw such further amounts as may be required to pay for purchases of silver bought for coinage purposes.

"(3) To draw such further amounts as an unexpectedly prosperous season may enable the Government to spare, to be used towards the reduction or avoidance of debt in England.

"(4) To sell additional bills and transfers to meet the convenience of trade.

" (5) To issue telegraphic transfers on India in payment for sovereigns which the Secretary of State has purchased in transit from Australia or from Egypt to India." The result of such drawings is that the councils are made to play an enormous part in the adjustment of the trade balance of India and the swelling of balances in the Home Treasury and the locking up of Indian funds in London.

The second point to note in comparing the preceding tables is with regard to the price at which the Secretary of State makes his sales. Before the closure of the Mints the price of the council bills was beyond the control of the Secretary of State, who had therefore to accept the price offered by the highest bidder at the weekly sale of his bills. But it is objected that there is no reason why the Secretary of State should have continued the old practice of auctioning the rupee to the highest bidder when the closing of the Mints had given him the sole right of manufacturing it. Availing himself of his monopoly position, it is insisted, the Secretary of State should not have sold his bills below 1s. 4 1/8d. or 1s. 4 3/32d., which, under the ratio of 15 rupees to the sovereign, was for India the gold-import point. In practice the Secretary of State has willed away the benefit of his position, and has accepted tenders at rates below gold-import point, as may be seen from the minimum rates he has accepted for his bills.

It is said that if the council bills were sold in amounts required strictly for the purposes of the Home Treasury, and sold at a price not below gold-import point, gold would tend to be imported into India and would thus become part of the Indian currency media. As it is, the combined effect of the operations of the Secretary of State is said to be to lock up Indian gold in London. With the use or misuse of the Indian gold in London we are not here concerned. But those who are inclined to justify the India Office scandals in the management of Indian funds in London, and have offered their services to place them on a scientific footing, may be reminded that a practice on one side of Downing Street which Bagehot said could not be carried on on the other side of it without raising a storm of criticism, would require more ingenuity than has been displayed in their briefs. This much seems to have been admitted on both sides that the operations of the Secretary of State do prevent the importation of gold into India, not altogether, but to the extent covered by their magnitude. Now, those who have held that the ideal of the Fowler Committee has been defeated are no doubt right in their view that the narrowing of the Secretary of State's operation would lead to the importation of gold into India. But what justification is there for assuming that the imported gold would become a part of the currency of India ? The assumption that the abolition of the Secretary of State's financial dealings would automatically make gold the currency of India is simply a gratuitous assumption. Whether the imported gold would become current depends on quite a different circumstance.

The other explanation offered to explain the failure of the ideal of the Fowler Committee is the want of a Mint in India open to the free coinage of gold. The opening of the Mints to the free coinage of gold has been regarded as the most vital recommendation of the Fowler Committee ; indeed, so much so that the frustration of its ideal has been attributed to the omission by the Government to carry it out. The consent given by the Government in 1900 to drop the proposal under the rather truculent attitude of the Treasury has ever since been resented by the advocates of a gold currency. A resolution was moved in 1911 by Sir V. Thackersay, in the Supreme Legislative Council, urging upon the Government the desirability of opening a gold Mint for the coinage of the sovereign if the Treasury consented, and if not for the coinage of some other gold coin.

TABLE LII

balance of trade, council drawings

and imports

of gold after 1893

Years. |

Excess (+) or Deficiency (—) of Bills drawn as compared with

Budget Estimate. |

Home Charges. |

||||||

|

|

Gold. |

Silver. |

|

|

|

|

|

(1) |

(2) |

(3) |

(4) |

(5) |

(6) |

(7) |

(8) |

(9) |

|

£ 000,000 |

£ 000,000 |

£ |

£ |

£ |

|

s. d. |

|

1893-94 |

21,660,500 |

- .39 |

8.3 |

9,530,235 |

- 9,169,765 |

15,826,815 |

1,300,564 |

1 1.500 |

1894-95 |

25,765,000 |

- 2.7 |

3.4 |

16,905,102 |

- 94,898 |

15,707,367 |

1,503,124 |

1 0.000 |

1895-96 |

29,963,800 |

1.5 |

3.7 |

17,664,492 |

+

664,492 |

15,603,370 |

3,393,798 |

1 1-000 |

1896-97 |

21,333,100 |

1.4 |

3.5 |

15,526,547 |

- 973,453 |

15,795,836 |

2,832,354 |

1 1-781 |

1897-98 |

18,847,000 |

3.2 |

5.4 |

9,506,077 |

- 3,493,923 |

16,198,263 |

2,534,244 |

1 2-250 |

1898-99 |

29,560,700 |

4.3 |

2.6 |

18,692,377 |

+

2,692,377 |

16,303,197 |

3,145,768 |

1 3-094 |

1899-1900 |

25,509,600 |

6.3 |

2.4 |

19,067,022 |

+

2,067,022 |

16,392,846 |

3,330,943 |

1 3-875 |

1900-01 |

20,727,400 |

.5 |

6.3 |

13,300,277 |

- 3,139.723 |

17,200,957 |

4,091,926 |

1 3-875 |

1901-02 |

28,630,600 |

1.3 |

4.8 |

18,539,071 |

+

2,039,071 |

17,368,655 |

6,693,137 |

1 3-875 |

1902-03 |

33,352,600 |

5.8 |

4.6 |

18,499,946 |

+

1,999,946 |

18,361,821 |

5,767,787 |

1 3-875 |

1903-04 |

45,424,100 |

6.6 |

9.1 |

23,859,303 |

+

6,859,303 |

18,146,474 |

7,294,782 |

1 3-875 |

1904-05 |

40,548,200 |

6.5 |

8.9 |

24,425,558 |

+

7,925,558 |

19,463,757 |

10,262,581 |

1 3-969 |

1905-06 |

39,086,700 |

.3 |

10.5 |

32,166,973 |

-1-14,333,973 |

18,617,465 |

8,436,519 |

1 3-938 |

1906-07 |

45,506,600 |

9.9 |

16.0 |

33,157,196 |

+15,357,196 |

19,208,408 |

5,606,812 |

1 3-969 |

1907-08 |

31,640,000 |

11.6 |

13.0 |

16,232,062 |

- 1,867,938 |

18,487,267 |

5,738,489 |

1 3-906 |

1908-09 |

21,173,300 |

2.9 |

8.0 |

13,915,426 |

- 4,584,574 |

18,925,159 |

8,453,715 |

1 3-906 |

1909-10 |

47,213,000 |

14.5 |

6.3 |

27,096,586 |

+10,896,586 |

19,122,916 |

15,809,618 |

1 3-906 |

1910-11 |

53,685,300 |

16.0 |

5.8 |

26,783,303 |

+11,283,303 |

19,581,563 |

18,174,349 |

1 3-906 |

1911-12 |

59,512,900 |

25.1 |

3.6 |

27,058,550 |

+

9,900,250 |

19,957,657 |

19,463,723 |

1 3-937 |

1912-13 |

57,020,900 |

22.6 |

11.5 |

25,759,706 |

+10,259,706 |

20,279,572 |

9,789,634 |

1 3.969 |

1913-14 |

43,753,900 |

15.6 |

8.7 |

31,200,827 |

+10,000,827 |

20,311,673 |

3,157,732 |

1 3.937 |

1914-15 |

29,108,500 |

5.1 |

5.9 |

7,748,111 |

-12,251,889 |

20,208,598 |

7,913,236 |

1 3-937 |

1915-16 |

44,026,600 |

- -7 |

3.-2 |

20,354,517 |

+13,354,517 |

20,109,094 |

12,803,348 |

1 3-937 |

1916-17 |

60,843,200 |

8.82 |

12.5 |

32,998,095 |

+29,093,095 |

21,145,627 |

11,391,993 |

1 4-031 |

1917-18 |

61,420,000 |

16.8 |

12.7 |

34,880,682 |

+34,880,682 |

26,065,057 |

16,625,416 |

1 4-156 |

1918-19 |

56,540,000 |

- 3.7 |

45.3 |

20,946,314 |

+20,946,314 |

23,629,495 |

14,715,827 |

1 4-906 |

In deference to the united voice of the Council, the Government of India again asked the Secretary of State to approach the Treasury for its sanction.[f32] The Treasury on this occasion presented the Secretary of State [f33]with two alternatives : (1) That a branch of the Royal Mint be established at Bombay solely for the purpose of coining gold into sovereigns, and exclusively under its control ; or (2) that the control of the Mint at Bombay should be entirely transferred to it. Neither of the two alternatives was acceptable to the Government of India ; and the Secretary of State, as a concession to Indian sentiment, sanctioned the issue of a ten-rupee gold coin from the Indian Mint. The Government of India preferred this solution to that suggested by the Treasury, but desired that the matter be dealt with afresh by the Chamberlain Commission then sitting. That Commission did not recommend a gold Mint,[f34] but saw no objection to its establishment provided the coin issued was a sovereign, and if the coinage of it was desired by Indian sentiment and if the Government did not mind the expense of coinage.[f35] This view of the Commission carried the proposition no further than where it was in 1900, until the war compelled the Government to open the Bombay Mint for the coinage of gold as a branch of the Royal Mint. But it was again closed in 1919. Its reopening was recommended by the Currency Committee of 1919 [f36], and so enthusiastically was the project received that an Honourable Member of the Supreme Council took the unique step of tempting the Government into adopting that recommendation by an offer to increase the Budget Estimates under " Mint " to enable the Government to bear the cost of it. The Government, however, declined the offer with thanks so we have in India the singular spectacle of a country in which there was a Gold Mint even when Gold was not legal tender, as was the case between 1835-93, while there is no gold Mint, when gold is legal tender, as has been the case since 1893. Just what an open Mint can do in the matter of promoting the ideal of the Fowler Committee it is difficult to imagine; but the following extracts from the evidence of a witness (Mr. Webb), than whom there was no greater advocate of an open gold Mint before the Chamberlain Commission, help to indicate just what is expected from a gold Mint.

" The principal advantage which you would expect to derive from a gold Mint is that you would increase the amount of gold coin in circulation ?—That would be one of the tendencies.

" Is there any other advantage ?—The advantage is that the country would be fitted with what I regard as an essential part of its monetary mechanism. I regard it as an essential part of its currency mechanism that it should have a Mint at which money could be coined at the requisition of the public.

" I want to get exactly at your reason why that is essential. Am I right in thinking that you consider it essential to a proper currency system that there should be a gold currency ?— Yes.

"And essential to a gold currency that there should be a gold Mint ?—Yes, on the spot in India itself...... It would do away, in a measure, with the management by the Secretary of State of the Foreign Exchanges, in that there would be always the Mint at which the public could convert their gold into legal-tender coins in the event of the Secretary of State taking any action of which the public did not approve. It is a safeguard, so to speak, an additional safeguard, that the people of India can on the spot obtain their own money on presentation of the metal."

Here, again, the assumption that a gold Mint is a guarantee that there will be a gold currency seems to be one as gratuitous as the former assumption that if gold were allowed to be freely imported it would on that account become part of the currency. On the other hand, there are cases where Mints were open, yet there was neither gold coinage nor gold currency. Instances may be cited from the history of the coinage at the Royal Mint in London. The magnitude of gold coinage during the bank suspension period, 1797-1821, or the late war, 1914-18, is instructive from this point of view. The Mint was open in both cases, but what was the total coinage of gold ?Throughout the suspension period the gold coined was negligible, and during the years 1807, 1812, and 1814-16 no gold was coined at all at the Royal Mint.[f37] Again, during the late war the coinage of gold fell off from 1915, and from 1917 it ceased altogether. [f38]

These instances conclusively show that although a Mint is useful institution, yet there is no magic in a Mint to attract gold to it. The historical instances adduced above leave no doubt that the circulation of gold is governed by factors quite independent of the existence or non-existence of a Mint open to the free coinage thereof.

Now, it is an established proposition of political economy that when two kinds of media are employed for currency purposes the bad one drives out the good one from circulation. Applying this principle to the situation in India, it should be evident that so long as there is an unlimited issue of rupees gold cannot circulate in India. This important principle has been so completely overlooked by those who have insisted on the introduction of a gold currency that they have not raised a finger against the unlimited issue of rupees. Mr. Webb, the fiercest opponent of the India Office malpractices, and the staunchest supporter of the view that if only the Secretary of State could be made to contract his drawings gold would flow and be a part of the currency in India, recommended to the Chamberlain Commission that—

"The sales of Council Drafts should be strictly limited to the sum required to meet the Home Charges, and no allotments should in any circumstances be made below, say, 1s. 4 1/8d. to 1s. 4 3/32 d.—i.e. about the present equivalent of specie point for gold imports into India. The sum required in London for Home Charges having been realised, no further sales of Council Drafts should be made except for the express purpose—duly notified to the public—of purchasing metal for the manufacture of further token coinage. Such special sales of Council Drafts should not be made at anything below specie point for gold imports[f39]."

Again, Sir V. Thackersay, in the course of his speech on March 22, 1912, moving a resolution in the Legislative Council, asking the Government to open the Mint for the coinage of gold in India, observed :—

" Let me make myself clear on one point. / do not suggest that Government should give up the right to coin rupees or refuse to give rupees when people demand the same. I do not propose to touch the gold-standard reserve, which must remain as it is as the ultimate guarantee of our currency policy. My proposal does not interfere with the existing arrangements in any way, but is merely supplementary to them...... Let the Government of India accumulate gold to the maximum limit of its capacity, but let the surplus gold which it cannot absorb be coined and circulated if the public chooses to do so. With our expanding trade and the balance in our favour, gold will continue to be imported in ordinary time, and if the facilities of minting are provided in India, it will go into circulation. "[f40]

These are surely not the ways of promoting a gold currency. Indeed, they run counter to it. So long as the coinage of rupees goes on gold will not enter into currency. Indeed, to cry out on the one hand against the huge drawings of the Secretary of State and the consequent transfer of Indian funds to London and their mismanagement by the Secretary of State, and on the other hand to permit him to manufacture additional token coinage of rupees, is to display not only a lamentable ignorance of a fundamental principle of currency, but also to show a complete failure to understand the precise source from which the whole trouble arises. It is true that the Government of India cannot bind the Secetary of State to any particular course of action [f41], and he often does override the provisions of the Annual Budget. But the question remains. How is it that he is able to draw so much more after 1893 than he ever did before ? It must be remembered that whatever the Secretary of State does with the funds in London he must pay for his drawings in India. Before 1893 he drew less because his means of payment were less ; after 1893 he drew more because his means of payment were greater. And why were his means of payment greater ? Simply because he had been able to coin rupees. Indeed, the amount of drawings are limited by the demand for them and by his capacity to coin rupees. It is therefore foolish to blame the Secretary of State for betraying the interests of India and at the same time to permit him to coin rupees, the very means by which he is able to betray. If a gold currency is wanted, and it is wanted because the rupee is a bad standard of value, then what is necessary is not to put a limit on the drawings of the Secretary of State or the opening of a gold Mint, but a short enactment stopping the coinage of rupees. Then only gold—made legal tender, at a suitable ratio with the rupee—will become a part of Indian currency.

That the stoppage of rupee coinage is a sufficient remedy is amply corroborated by the now forgotten episode in the history of Indian currency during the years 1898-1902. Within the short space of a year and a half after gold had been made legal tender the Hon. C. E. Dawkins, notwithstanding the fact that there was no gold Mint, was able, in his Budget speech in March, 1901, to observe:—

" India has at length emerged from a period of transition in her currency, has reached the goal to which she has been struggling for years, has established a gold standard and a gold currency, and has attained that practical fixity in exchange which has brought a relief alike to the private individual and to the Government finances."[f42] So great was the plethora of gold that Mr. Dawkins further remarked [f43]—

"...... We have been nearly swamped...... by gold......." The transformation in the currency position which then took place was graphically described by Lord Curzon, the then Viceroy, in the following words[f44]':—

"Mr. Dawkins...... has successfully inaugurated the new era under which the sovereign has become legal tender in India, and stability in exchange has assumed what we hope may be a stereotyped form. This great change has been introduced in defiance of the vaticinations of all the prophets of evil, and more especially of the particular prophecy that we could not get gold to come to India, that we could not keep it in our hands if we got it here, but that it would slip so quickly through our fingers that we should have even to borrow to maintain the necessary supply. As a matter of fact, we are almost in the position of the mythological king, who prayed that all he touched might be turned into gold, and was then rather painfully surprised when he found that his food had been converted into the same somewhat indigestible material. So much gold, indeed, have we got, that we are now giving gold for rupees as well as rupees for gold, i.e. we are really in the enjoyment of complete convertibility—a state of affairs which would have been derided as impossible by the experts a year ago."

Compare this state of affairs in 1900-1 with that found to exist in 1910-11, for instance. Speaking of the currency situation as it was in that year, the Hon. Sir James (now Lord) Meston, observed[f45]:—

" We have passed through many changes in currency policy and made not a few mistakables. but the broad lines of our action and our objects are clear and unmistakable, and there has been no great or fundamental sacrifice of consistency in progress towards our ideal. Since the Fowler Committee that progress has been real and unbroken. There is still one great step forward before the ideal can be reached. We have linked India with the gold countries of the world, we have reached a gold-exchange standard, which we are steadily developing and improving. The next and final step is a true gold currency. That, I have every hope, will come in time......"

Leaving aside for the moment the extenuatory remarks of the speaker, the fact remains that in 1900 India had a gold currency. But, taking stock of the position at the end of 1910, it had ceased to have it. What is it that made this difference ? Nothing but the fact that between 1893-1900 no rupees were coined, but between 1900-1910 the number of rupees coined was enormous. During the first period the inducement to coin rupees was very great indeed. The exchange was not quite stable, and the Government had still to find an increasing number of rupees to pay for the " Home Charges." And an Honourable Member[f46] of the Supreme Legislative Council actually asked:—

" Is there any objection to the Government working the Mints on their own account ? Considering the low value of

silver and the great margin between the respective prices of bullion and the rupee, would not Government by manufacturing rupees for itself make sufficient profit to meet at least a substantial portion of the present deficit ? It seems to me to be a legitimate source of revenue and one capable of materially easing our finances."

But Sir James Westland, who was then in charge of the finances of India, replied[f47] :—

" I must confess to a little surprise in finding the proposal put forward by one of the commercial members of your Excellency's Council that we should buy silver at its present low price, and coin it for issue at the appreciated value of the rupee...... I shall certainly refuse myself to fall into this temptation."

Again, 1898, when some of the followers of Mr. Lindsay desired that Government should coin rupees to relieve the monetary stringency, Sir James Westland remarked [f48] :—

"...... in our opinion the silver standard is now a question of the past. It is a case of vestigia nulla retrorsum. The only question before us is how best to attain the gold standard. We cannot go back to the position of the open Mints. There are only two ways in which we can go back to that position. We can either open the Mints to the public generally, or we can open them to coinage by ourselves. In either case what it means is that the value of the rupee will go down to something approaching the value of silver. If the case is that of opening the Mints to the public, the descent of the rupee will be rapid. If it is that of opening only to coinage by the Government, the descent of the rupee may be slow but it will be no less inevitable."

The Hon. C. E. Dawkins was equally emphatic in his denunciation of the project of Government coining rupees. When he was tempted to acquiesce in the proposal by holding out the prospects of a profit from coinage, he replied[f49]:— "I think I ought...... to beg my hon. friend not to dangle the profits on silver too conspicuously before the eyes even of a most virtuous government. Once let these profits become a determining factor in your action, then good-bye stability." Another instance of the Government's determination not to coin rupees is furnished by inquiring into the reasons as to why it is that the Government has never assumed the responsibility of selling council bills in indefinite amount and at a fixed rate. The Chamberlain Commission argued that the Government cannot undertake such a responsibility because it cannot hold out for a fixed rate, and may have to sell at any rate even lower than par. This is true so far as it is a confession of a position weakened by the Government's folly of indulging in excessive rupee coinage. But this was certainly not the explanation which the Government gave in 1900 when it was first asked to assume that responsibility. The Government knew perfectly well that to keep on selling bills indefinitely was to keep on coining rupees indefinitely. They refused to assume that responsibility because they did not want to coin rupees. That this was the original reason was made quite plain by the Hon. Mr. Dawkins, [f50]who reminded those who asked Government to undertake such a responsibility that "the silver coin reserve of Government in consequence rapidly neared a point at which it was impossible to continue to meet unlimited transfers [i.e. council bills]. Therefore the Secretary of State decided to limit the demands by gradually raising the rate, thus meeting the most urgent demands, and weeding out the less urgent, while warning those whose demands were not so urgent to ship gold to India. No other course was practicable. The liability of the Secretary of State to keep the tap turned on indefinitely at 1s. 4 5/32d. has been asserted. But I cannot see that any positive liability exists, and I wonder if those who assert its existence would have preferred that the stability of our currency (whose situation they are well able to appreciate and follow) should have been affected by the reserve of rupees being dangerously reduced ?" [and which could not be augmented except by coining more rupees].

Just at the nick of time, when the ideal of a gold standard with a gold currency was about to be realised, there came on the scene Sir Edward Law as the Finance Minister of India and tore the whole structure of the new currency to pieces with a piratical nonchalance that was as stupid as it was wanton. His was the Minute of June 28, 1900, which changed the whole course of events.[f51] In that Minute occurs the following important passage;—

"15. As a result of these considerations it must, I think, be admitted that the amount of gold which can safely be held in the currency reserve must for the present be regulated by the same rules as would guide the consideration of the amount by which the proportion invested in government securities could be safely increased. Pending an increase in the note circulation...... or some other change in existing conditions, I am of opinion that a maximum sum of approximately £ 7,000,000 in gold may now be safely held in the currency reserve. I should not, however, wish to be bound absolutely to this figure, which is necessarily an arbitrary one, and particularly I should not wish any public announcement to be made which might seem to tie the hands of the Government in the event of circumstances, at present unforeseen, rendering its reduction hereafter desirable."

In outlining this Minute, which with modifications in the maximum gold to be held in the currency reserve, remains the foundation of the currency system in India, the author of it never seems to have asked for one moment what was to happen to the ideal of a gold standard and a gold currency ? Was he assisting the consummation of the gold standard or was he projecting the abandonment of the gold standard in thus putting a limit on the holding of gold ? Before the policy of this Minute was put into execution the Indian currency system was approximating to that of the Bank Charter Act of 1844, in which the issue of rupees was limited and that of gold unlimited. This Minute proposed that the issue of gold should be limited and that of rupees unlimited—an exact reversal to the system of the Bank Suspension period. In this lies the great significance of the Minute, which deliberately outlined a policy of substituting rupees for gold in Indian currency and thereby defeating the ideal held out since 1893 and well-nigh accomplished in 1900.

If Sir Edward Law had realised that this meant an abandonment of the gold standard, perhaps he would not have recorded the Minute. but what were the considerations alluded to in the Minute which led him thus to subvert the policy of a gold standard and a gold currency and put a limit on the gold part of the currency rather than on the rupee part of the currency ? They are to be found in a despatch, No. 302, dated September 6, 1900, from the Government of India, which says:—

"2. ...... the receipts of gold continued and increased after December last. For more than eight months the gold in the currency reserve has exceeded, and the silver has been less, than the limits suggested in the despatch of June 18. By the middle of January the stock of gold in the currency reserve in India reached £5,000,000. The proposal made in that despatch was at once brought into operation; later on we sent supplies of sovereigns to the larger District Treasuries, with instructions that they should be issued to anyone who desired to receive them in payments due or in exchange for rupees; and in March we directed the Post Office to make in sovereigns all payments of money orders in the Presidency towns and Rangoon, and we requested the Presidency Banks to make in the Presidency towns and Rangoon payments on Government account as far as possible in sovereigns. These measures were taken, not so much in the expectation that they would in the early future relieve us of any large part of our surplus gold, but in the hope that they would accustom the people to gold, would hasten the time when it will pass into general circulation in considerable quantities, and by so doing, would mitigate in future years the difficulties that we were experiencing from the magnitude of our stock of gold and the depletion of our stock of rupees.

"3. In order to meet these difficulties and to secure, if possible, that we should have enough rupees for payment to presenters of currency notes and tenderers of gold, we began to coin additional rupees......

*****

"14. We may mention that we have closely watched the result of the measures described in paragraph 2. The issues of gold have been considerable; but much has come back to us through the Currency Department and the Presidency banks. The Comptroller-General estimated the amount remaining in circulation at the end of June at over a million and a quarter out of nearly two millions issued up to that time ; but there are many uncertain data in the calculation. We are not yet able to say that gold has passed into use as money to any appreciable extent.

"15. It is very desirable that we should feel assured of being able to meet the public demand for rupees, as indicated by the presentation of currency notes and gold. We therefore strongly press on your Lordship the expediency of sanctioning

the above proposal for further coinage [of rupees];...

*****

"17. But we do not wish our proposal to be considered as dependent on such arguments as those just stated. We make it primarily on the practical ground that we consider it necessary in order to enable us to fulfil an obligation which, though we are not, and do not propose to be, legally committed thereto, we think it desirable to undertake so long as we can do it without excessive inconvenience; namely, to pay rupees to all tenderers of gold and to give rupees in encashment of currency notes to all who prefer rupees to sovereigns."

The arguments advanced in this statement of the case for coining rupees are a motley lot. At the outset it is something unheard of that a Government which was proceeding to establish a gold standard and a gold currency should have been so very alarmed at the sight of increased gold when it should have thanked its stars for such an early consummation of its idea. Leaving aside the psychological aspect of the question, the government, according to its own statement, undertook to coin rupees for two reasons: (1) because it felt itself obliged to give rupees whenever asked for, and (2) because people did not want gold. What force is there in these arguments ? Respecting the first argument it is difficult to understand why Government should feel itself obliged to give rupees. The obligation of a debtor is to pay the legal-tender money of the country. Gold had been made legal tender, and the Government could have discharged its obligations by paying out without shame or apology. Secondly, what is the proof that people did not want gold ? It is said that the fact that the gold paid out by Government returned to it is evidence enough that people did not want it. But this is a fallacy. In a country like India Government dues form a large part of the people's expenditure, and if people used that gold to meet those dues—this is what is meant by the return of gold to Government—then it is an evidence in support of the contention that people were prepared to use gold as currency. But if it is true that people do not want gold, how does it accord with the fact that Government refuses to give gold when people make a demand for it ? Does not the standing refusal imply that there is a standing demand ? There is no consistency in this mode of reasoning. The fact is, all this confused advocacy is employed to divert attention from the truth that the Government was anxious to coin rupees not because people did not want gold, but because Government was anxious to build a gold reserve out of the profits of additional coinage of rupees. That this was the underlying motive is manifest from the minute of Sir Edward Law. That the argument about people disliking gold, and so forth, and so forth, was only a cover for the true motive comes out prominently from that part of the Minute in which its author had argued that —

"16. If it be accepted that £ 7,000,000 is the maximum sum which, under existing conditions, can be held in gold in the currency reserve, in addition to the 10 crores already invested, it is evident that such assistance as can be obtained from manipulating the reserve will fail to provide the sum in gold which it is considered advisable to hold in connection with the maintenance of a steady exchange. So far no authority has ventured to name a definite sum which should suffice for this purpose, but there is a general consensus of opinion, in which I fully concur, that a very considerable sum is required. The most ready way of obtaining such a large sum is by gold borrowings, but the opinion of the Currency Commission was strongly hostile to such a course, and the question therefore remains unanswered : How is the necessary stock of gold to be obtained ?

"17. I do not presume to offer any cut-and-dried solution of this difficult problem, but I venture to offer certain suggestions which, if adopted, would, I believe, go a considerable way towards meeting the difficulty. I propose to create a special ' Gold Exchange Fund,' independent of, but in case of extraordinary requirements for exchange purposes to be used in conjunction with the gold resources of the currency reserve. The foundation of this fund would be the profit to be realised by converting into rupees the excess above £7,000,000 now held in gold in the currency reserve."

Can there be any doubt now as to the true cause for coining rupees ? Writers who have broadcasted that rupees were coined because people did not want gold cannot be said to have read correctly the history of the genesis of the exchange standard in India.

But was Sir Edward Law the evil genius who turned a sound system of currency into an unsound one by his disastrous policy of coining rupees ? Opponents of the Government as well as its supporters are all agreed[f52]that this was a departure from the ideal of the Fowler Committee. In what precise respect the Government has departed from the recommendations of the Fowler Committee has, however, never been made clear anywhere in the official or non-official literature on the subject of Indian currency. What were the recommendations of the Fowler Committee ? It is usually pointed out, to the shame of the Government of India, that the Fowler Committee had said (it is as well to repeat it) :—

" We are in favour of making the British sovereign a legal tender and a current coin in India. We also consider that, at the same time, the Indian Mints should be thrown open to the unrestricted coinage of gold...... Looking forward as we do to the effective establishment of a gold standard and currency based on the principles of the free inflow and outflow of gold, we recommend these measures for adoption."

That is true. But those who have blamed the Government have forgotten that same Committee also recommended that—

"The exclusive right to coin fresh rupees must remain vested in the Government of India; and though the existing stock of rupees may suffice for some time, regulations will ultimately be needed for providing such additions to the silver currency as may prove necessary. The Government should continue to give rupees for gold, but fresh rupees should not be coined until the proportion of gold in the currency is found to exceed the requirements of the public. We also recommend that any profit on the coinage of rupees should not be credited to the revenue or held as a portion of the ordinary balance of the Government of India, but should be kept in gold as a special reserve, entirely apart from the paper-currency reserve and the ordinary Treasury balances " [and be made freely available for foreign remittances whenever the exchange falls below specie point.]

Taking the two recommendations of the Committee together, where is the departure ? What the Government has done is precisely what the Committee had recommended. That the Government of India or the Chamberlain Commission should have admitted for a moment that there was a departure is not a little odd, for the very despatch which conveyed the Minute of Sir Edward Law to the Secretary of State opens with remarks which show that Government was earnestly following the recommendations of the Fowler Committee. It runs:—

"In our despatch No. 301 of August 24, 1899, we wrote with reference to paragraph 60 of the Report of the Indian Currency Committee [i.e. the Fowler Committee], that any profit made on rupee coinage should be held in gold as a special reserve, has not escaped our attention ; but the need for the coinage of additional rupees is not likely to occur for some time, and a decision on this point may be conveniently deferred."